Turning 65 means you become eligible for Medicare, a federal health insurance program for senior citizens. Medicare offers two main options for coverage – Original Medicare and Medicare Advantage. However, Original Medicare does not cover all expenses. You may need additional coverage to pay for things like copays, deductibles, and coinsurance.

To offset these expenses, many individuals opt for either Medicare Supplement Insurance (also known as Medigap). They can also choose a Medicare Advantage plan (also known as Part C). Each of these options works differently. So it is essential to understand which one is most suitable for your specific needs and circumstances.

With so many options available, it is challenging to decide between Medicare Advantage and Medigap. HPO is available to provide assistance and help you get started.

Watch explainer video here >>>

What is Medicare Supplement Insurance?

![]()

This type of insurance works in conjunction with your Original Medicare coverage and helps pay for services that are not covered by Part A and Part B. These services include foreign travel and excess charges, such as when a doctor does not accept Medicare. Medigap can also assist with the cost of your Part A deductible, which is $1,556 for 2022, as well as the 20% coinsurance rates associated with Part B coverage.

It’s important to note that Medicare Supplement Insurance is not a stand-alone coverage plan. You must first be enrolled in Original Medicare. Additionally, Medigap does not include coverage for prescription medications. To obtain this coverage, you will need a third plan – Medicare Part D.

There are ten different Medigap insurance plans available, including Plans A through D, F and G, and K through N. However, Plans C and F are not available to individuals who enrolled in Medicare after January 1, 2020. Medigap insurance plans generally cover 100% of your Part A coinsurance costs and many plans cover 100% of your Part B coinsurance and copayment costs.

If you opt for Medigap, keep in mind that it will come with a monthly premium. The amount varies based on your chosen plan and could be several hundred dollars per month. Additionally, some plans may have deductibles and copays.Medigap plans do not include additional benefits such as dental, vision, over the counter items, and other coverage that is above and beyond what original Medicare provides.

What is a Medicare Advantage plan?

Medicare Advantage, or MA, is a healthcare plan that you can choose instead of Original Medicare. MA plans are provided by private insurance companies and offer the same coverage as Parts A and B, but usually also include Part D and additional benefits like routine dental, hearing, and vision services all in one policy.

By law, Medicare Advantage plans cover the same types of medical services as Original Medicare, including hospital services, doctor appointments, and lab tests. However, you may have to stay within a certain network or get a referral from your primary care physician before the plan will pay for the costs.

If you enroll in Medicare Advantage, your benefits will be administered through the private plan, which will replace your Original Medicare coverage. You will not be able to enroll in a Medicare Supplement plan or a stand-alone Part D plan.

Many Medicare Advantage plans do not charge an additional premium beyond the usual Part B premium. However, you may still have to pay a deductible, copays, and coinsurance. MA plans generally have an annual out-of-pocket maximum, which limits the amount you have to spend each year.

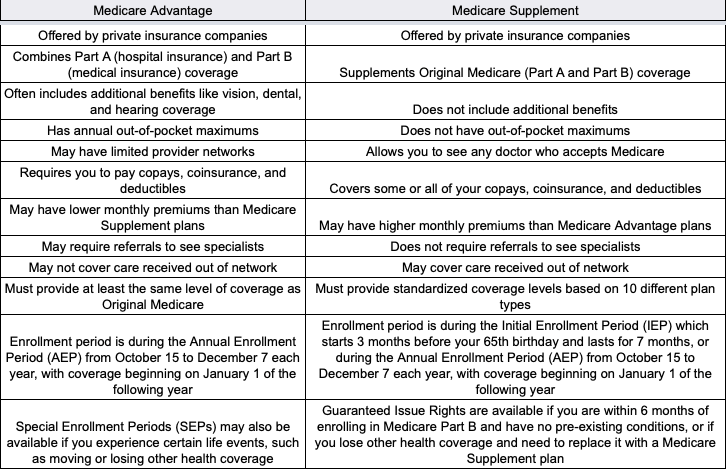

Medicare Advantage vs. Medicare Supplement Insurance: Comparison chart

Let’s take a quick overview of the difference between Medicare Advantage and Medicare Supplement Insurance.

Medicare Advantage vs Medicare Supplement comparison chart